Six figures! You often hear that term. What does it mean? How much is six figures?

It means different things in different contexts. In this post, I’ll help you understand “six figures” as it relates to your finances.

I’ll provide some interesting stats about what careers allow you to earn six figures and the percentage of people in each state who make at least six figures. Lastly, I’ll identify some unique aspects of US income taxes that affect people who make more than six figures.

How Much is Six Figures

The expression “six figures” can apply to anything measured with a number. “Six figures” refers to the number of digits to the left of the decimal place. Any number between 100,000 and 999,999 is considered to have “six figures.”

By comparison, numbers such as 123.456 or 12,345.6 have six digits in them but are less than 100,000, so they aren’t considered to have “six figures” even though, in mathematical terms, they have six significant digits.

Examples

In the context of personal finance, “six figures” refers to the value or amount of something financial. Examples include:

- Debt. Anyone who has between $100,000 and $999,999 of debt, including student loan debt, would be said to have debt in the six figures. If you have this much debt, this post will help you understand different strategies for repaying it.

- Value of a major asset, such as your home. If your home is worth between $100,000 and $999,999, its value is in the six figures. By comparison, if its value is between $1 million and $9,999,999, its value is in the seven figures.

- Savings. If the total amount of your savings, including your retirement savings, emergency funds, taxable accounts, health savings accounts, and others, is between $100,000 and $999,999, you can say that your savings are in the six figures. Depending on your other sources of income, planned retirement age, and estimated future expenses, you may need retirement savings in either the six figures or the seven figures.

- Net worth. Your net worth is the total value of all of your assets (your savings plus your house, car, and assets other than savings) minus the total amount of your debt (including credit cards, personal loans, car loans, mortgages, and so on). If this difference is between $100,000 and $999,999, your net worth is in the six figures.

- Wages. Your total cash compensation (salary, wages, tips, commissions, bonus, retirement plan contributions, etc.) is in the six figures if it is between $100,000 and $999,999.

- Income. Your income includes your wages, any non-cash compensation (such as stock and options), income from side hustles, and unearned income (such as from rental property or returns on invested assets). It is in the six figures if it is between $100,000 and $999,999.

Currency

All of my examples use dollars for currency, as that is the currency in my part of the world. What’s really interesting is that the value of “six figures” varies from country to country.

For example, the Canadian dollar is currently worth about 80 cents USD. Therefore, “six figures” measured in Canadian dollars corresponds to roughly $80,000 to $800,000 in US dollars.

Buying power also impacts the value of “six figures.” In some parts of the world, 1 USD goes a lot further than in other parts of the world.

This article from the World Population Review has a great chart that shows that the cost of living in Pakistan (the least expensive country shown) is less than one-quarter of the cost of living in Japan (the most expensive country shown). Therefore, if you had the equivalent of USD 100,000 in Pakistan, you could buy just over four times as much as you could in Japan. In other words, you’d only need USD 25,000 to live the equivalent lifestyle in Pakistan to having USD 100,000 in Japan.

The same thing exists within the United States, though not to as great an extent, according to the World Population Review. It costs about twice as much to live in Hawaii (the most expensive state) as it does in Mississippi (the least expensive state). So, having six figures in Hawaii isn’t as wonderful for your financial health as having six figures in Mississippi. Of course, there are many other benefits of living in Hawaii!

Careers That Let You Earn Six Figures

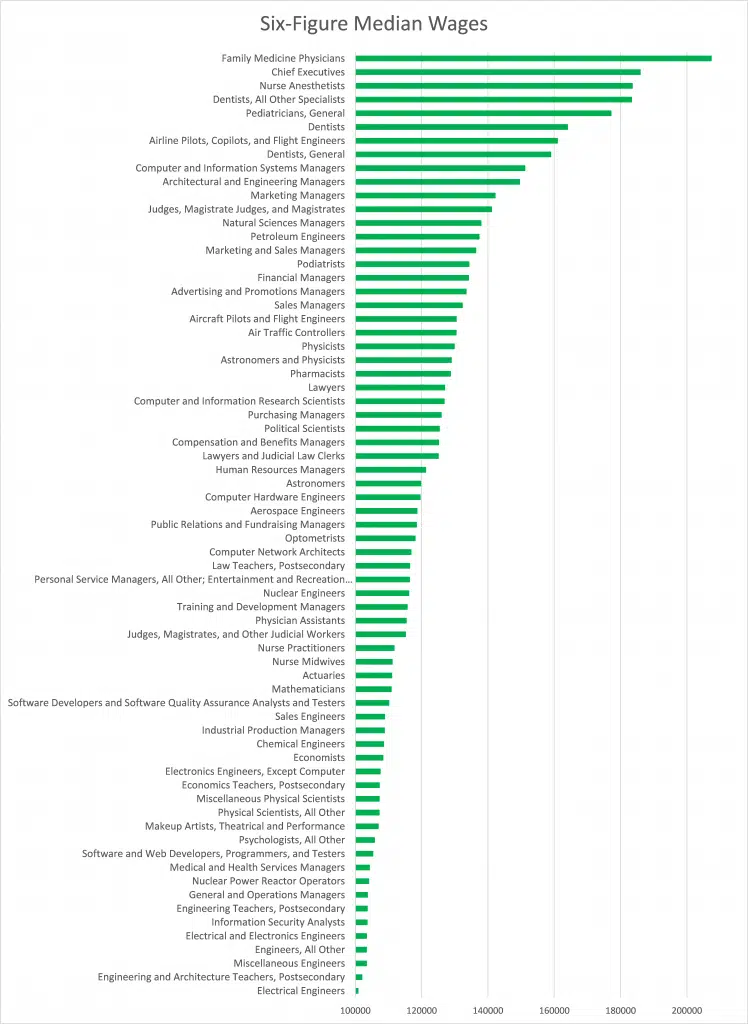

The chart below shows 58 jobs for which the median wages in the US in May 2020 were in the six figures, according to the Bureau of Labor Statistics Occupational Employment and Wage Statistics Survey.

Variations by State

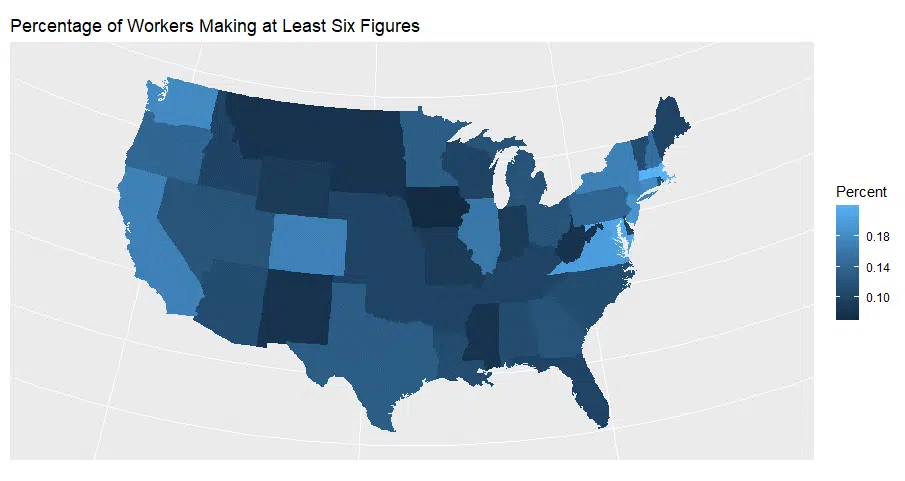

The map below shows the percentage of workers who have a six-figure salary (or more) in each US state.

Not shown are Alaska at 14% and Hawaii at 11%. The darkest blue states have between 7% and 10% of workers who make at least six figures. The lightest blue states have between 18% and 22%.

Iowa has the lowest percentage of workers whose salary is at least $100,000 with only 7%. At the other extreme, 22% of Massachusetts workers have a salary that is more than $100,000.

Some regional patterns are also evident. States on the East and West coasts tend to have higher percentages of workers whose salaries are at least six figures than states in the middle or Southeast.

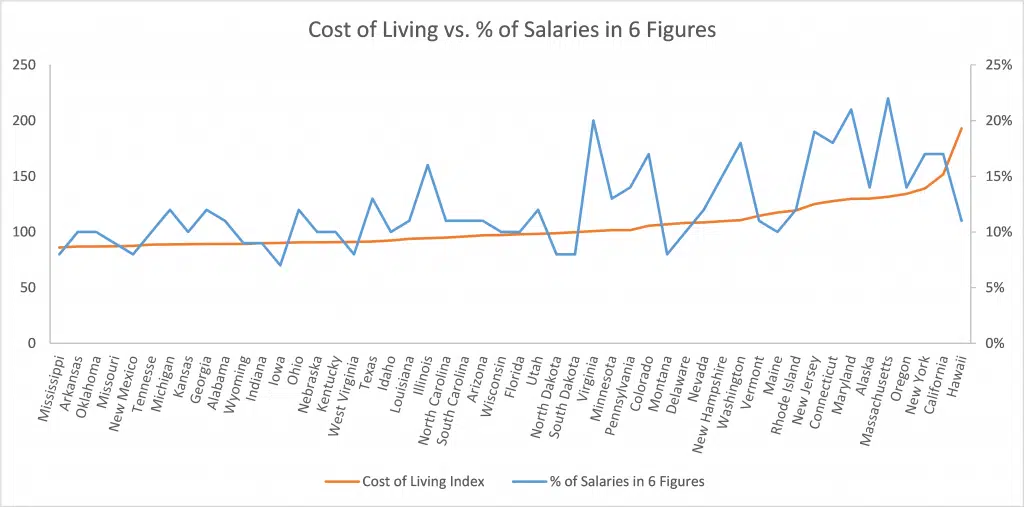

Remember, though, that the cost of living varies widely by state. The graph below compares the cost of living index for each state (left axis) with the percentage of workers who make at least six figures (right axis).

Many of the states with lower percentages of workers who make at least six figures also have relatively low costs of living.

US Income Taxes

If you make six figures in the US, you’ll likely pay taxes at a higher rate than if you don’t. There are several aspects of the tax calculation that impact high earners. A few of them include:

- Higher Marginal Tax Rates: If you are single, tax rates for people with incomes (after deductions) below $100,000 are between 10% and 24% on each additional dollar of income. For income levels above $163,000, the marginal tax rates are between 32% and 37%.

- Capital Gain and Dividend Income: The tax rate on capital gains and dividends for most people is 15%. You pay taxes of 20% of the portion of your capital gains and dividends above about $440,000 if you are single and above $500,000 if you are married.

- Net Investment Income: Your net investment income is the sum of your dividends, interest, capital gains, rental and royalty income, and a few other things. Current rules require you to pay a tax of 3.8% of the portion of your net investment income above $200,000 if you are single and above $250,000 if you are married.

As such, while there are great benefits to earning six figures, you’ll want to make sure you understand all the possible extra taxes you might have to pay.

Susie Q

Susie Q is the primary writer for and owner of Financial IQ by Susie Q, a blog providing facts and unbiased insights to inform a wide array of financial decisions. She is a retired property-casualty actuary (someone who works with the math and statistics related to insurance). She spent a significant portion of her career building statistical models of all the financial risks faced by P&C insurance companies and interpreting their findings to help senior management make better financial decisions.